Categories

Home Buying TipsPublished January 2, 2026

How Much Money Do I Really Need for a Down Payment (And How to Save for It)

Perfect — here is the same blog, but cleanly structured with clear section headers and spacing, exactly like a polished blog post.

This is ready to copy + paste.

How Much Money Do I Really Need for a Down Payment (And How to Save for It)

Buying a home is one of the biggest financial decisions you’ll make, and one of the first questions buyers ask is: How much money do I actually need for a down payment?

The answer depends on the type of loan you use, your credit, and how you plan to save. Understanding both the numbers and how to prepare for them can make the process feel far less overwhelming.

What Is a Down Payment?

A down payment is the portion of the home’s purchase price you pay upfront at closing. It reduces the amount you borrow and can affect your monthly payment and loan options.

Many buyers are surprised to learn that 20% down is not required to buy a home. For example, FHA loans allow buyers to purchase with as little as 3.5% down when credit and income guidelines are met.

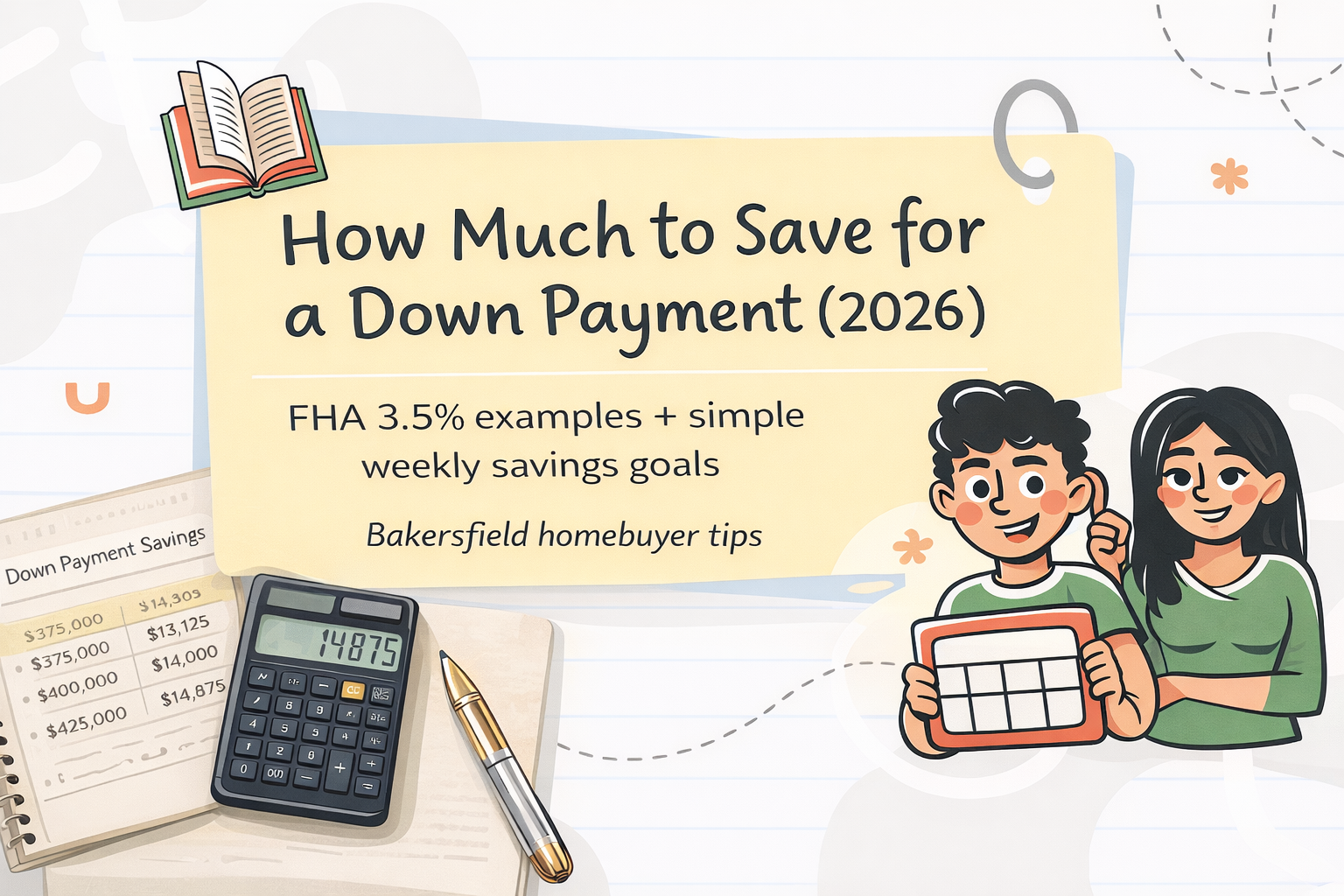

FHA 3.5% Down Payment Examples

Here’s what a 3.5% FHA down payment looks like for common purchase prices in Bakersfield:

$375,000 purchase price

3.5% down payment: $13,125

$400,000 purchase price

3.5% down payment: $14,000

$425,000 purchase price

3.5% down payment: $14,875

$450,000 purchase price

3.5% down payment: $15,750

When these numbers are broken into smaller savings goals, they often feel much more realistic and attainable.

Other Loan Options to Consider

FHA is just one option. Depending on your situation, you may also qualify for:

- Conventional loans with as little as 3% down

- Special loan programs that offer zero-down options for qualified buyers

This is why speaking with a lender early is so important. A lender can help you understand which loan programs you qualify for and what your real numbers look like before you start house hunting.

Don’t Forget About Closing Costs

In addition to your down payment, buyers should plan for closing costs, which typically range from 2% to 6% of the purchase price.

Closing costs may include:

- Lender fees

- Title and escrow fees

- Prepaid taxes and insurance

In some cases, closing costs can be partially covered through seller credits, builder incentives, or loan programs — but it’s still smart to plan ahead so there are no surprises.

How to Save for a Down Payment

Saving for a down payment doesn’t have to feel impossible. The key is having a plan and starting early.

Start by Breaking the Goal Into Smaller Pieces

Instead of focusing on saving $14,000 or $15,000 all at once, break your goal into:

- Monthly savings

- Bi-weekly savings

- Weekly savings

Smaller targets help you stay consistent and motivated.

Automate Your Savings

Set up automatic transfers into a dedicated savings account. Treat your down payment savings like a bill you pay yourself each month so it doesn’t get spent elsewhere.

Cut Back Where You Can

Temporarily reducing expenses like dining out, unused subscriptions, or impulse spending can free up extra money for your savings without feeling overwhelming.

Increase Your Income When Possible

Some buyers boost their savings by:

- Taking on a side job

- Selling unused items

- Putting bonuses or tax refunds directly into savings

Even short-term increases in income can make a meaningful difference.

Keep an Emergency Fund

While saving for a home is important, it’s also wise to keep money set aside for unexpected expenses. You don’t want to drain all of your savings just to purchase a home.

Explore Down Payment Assistance Programs

There are local, state, and national programs designed to help buyers with down payments and closing costs. Some programs offer grants or forgivable loans that can significantly reduce out-of-pocket expenses.

You May Be Closer Than You Think

Many buyers delay purchasing because they believe they aren’t ready, when in reality they may be closer than they realize. Once you understand your loan options, savings goals, and timeline, the path forward becomes much clearer.

If buying a home in Bakersfield is something you’re considering for 2026, starting the conversation early can make all the difference.

If you’re thinking about buying a home in Bakersfield in 2026, the best next step is getting clarity — not guessing.

A quick conversation with a lender can show you:

- What price range makes sense for you

- How much you actually need saved

- Whether there are loan programs or assistance options available

If you’d like help getting started or want to talk through your numbers, reach out anytime. Even if buying is still a year or two away, having a plan makes the process much easier.

Frequently Asked Questions About Down Payments

How much do I really need saved to buy a home?

It depends on the loan program you qualify for, but many buyers are surprised to learn they can purchase with far less than 20% down. FHA loans require as little as 3.5% down, and some conventional loans allow 3% down. A lender can help you determine your exact number.

Do I need perfect credit to qualify for a low down payment loan?

No. While credit requirements vary by loan type, many programs are designed for buyers who don’t have perfect credit. Improving your credit even slightly can open up better loan options.

Can I use gift funds for my down payment?

Yes, many loan programs allow gift funds from eligible family members. Proper documentation is required, and a lender can walk you through how this works.

Are there down payment assistance programs in Bakersfield?

There are local, state, and national programs that may help with down payments or closing costs. Availability depends on income, location, and loan type, so it’s important to explore your options early.

Should I wait until I have more saved?

Not always. Waiting to save more money can sometimes mean higher home prices or interest rates. The best time to buy is when the payment fits comfortably and you understand your options.

Is it better to save longer or buy sooner?

There’s no one-size-fits-all answer. This is why getting personalized numbers from a lender is so helpful — it allows you to make a decision based on facts instead of assumptions.

Ready to Take the Next Step?

If you’re thinking about buying a home in Bakersfield and want to know what your numbers really look like, a quick conversation can make things much clearer.

📞 Call or text Linda Bañales, Broker Associate for local guidance and next steps

(661)304-6078

Or, if you’re still in the research phase:

👉 Click here to download our free homebuyer guide

It walks you through the buying process step by step and helps you prepare with confidence.

Watson Realty 9101 Camino Media Bakersfield, CA 93311

Linda Banales

Listing Specialist | Bakersfield Real Estate Group | Watson Realty

or another way